Discounting definition. Discounting cash flows: what is it. Calculation of the discount rate based on the Gordon model

For people who do not have an economic education, the term “discounting” is most likely not even familiar. Moreover, when calculating the discount rate in assessing cash flows, the use of special formulas is required, so at first glance the concept looks quite complex. However, the discount rate has a certain economic essence and no special formulas are required to understand it. Let's try to talk about discounting and the discount rate in simple words.

The laws of economics say: money tends to depreciate. This was not always the case - but since the 1930s, money began to lose its status of constant value, subject to constant inflation. That is why it is important for an investor to understand what awaits him in the future, whether it makes sense to invest his capital in a certain asset - how profitable it is or, on the contrary, how risky it is. To evaluate the deposit, they resort to calculating the discount rate, which is needed to reassess the value of future capital at the current moment.

It doesn’t sound very simple, but we can give the following analogy: 1000 rubles today is not the same 1000 rubles in five years, since as a result it will be possible to buy a smaller quantity of goods. Those. the value of money will fall by a certain amount, most likely different if you divide five years into annual intervals. This value is the discount rate. The discounted value, in turn, shows what funds need to be owned (invested) in order to receive a certain known amount X in the future at a known rate.

What is the discount rate and cash flow?

In an investment context, the discount rate shows the level of expected return on an investment. When calculating the rate, the investor will compare the future value of the object, assessing it relative to the present time. It follows that the discount rate becomes the starting point for calculating the efficiency of an investment. Some economists refer to the discounting method as a process in which cash flows are compared - i.e. funds remaining at the disposal of a company after all operating expenses have been paid and necessary investments have been made.

The essence of the discounting technique on paper is quite simple. First, you should forecast the company's cash flows in the range of 5-10 years. This period will be called the forecast period. Next, using a special formula, you need to calculate the discount rate for each period. The final results need to be summed up to obtain a value that will indicate the likely level of profitability of the company in the coming years.

The easiest way to make such a calculation is where the profitability is known in advance - i.e. using the example of a bank deposit or bond payments. To begin with, we present the calculation formula that corresponds to the compound interest formula:

PV(t 0) - discounted value at the initial moment of time

FV(t) — future amount at time t

i- discount rate

Example. If we take a bank deposit with a yield of 5% per annum (corresponding to the discount rate) with a final amount of 1000 rubles, then the discounted value will be equal to 1000 / (1 + 0.05)¹ ≈ 952.4 rubles. If the amount of 1000 rubles at the same rate appears in two years, then the discounted value is calculated as 1000 / (1 + 0.05)² ≈ 907 rubles. However, the purchasing power of money will decrease over the year. If inflation was 4%, then in the case of an annual deposit we have: 1000 / 1.04 ≈ 961.5 rubles. Those. in reality, the purchasing power of our money at the end of the deposit period increased only by 961.5 - 952.4 ≈ 9 rubles (and could have decreased if inflation had exceeded 5%).

In the case of a bond, there are often several payments made during the year (every quarter) - therefore, in this case it is more appropriate to talk about the discounted value of the payment stream. The formula for calculation is very similar to that written above:

where CF(t) is the payment at time t, which for a bond could be the quarterly coupon income. Let's take the bond's yield to be 5% per annum, as in the previous case for the deposit. Then for an annual bond worth 1000 rubles, the payments are 12.5, 12.5, 12.5 and 1012.5 rubles with a total amount of 1050 rubles. Now let's take a discount rate of 4% in the form of expected inflation and discount the cash flow:

In total, the real value of our investment at the end of the bond’s validity period corresponds to 1010.33 rubles in today’s prices (if inflation really amounted to 4% per annum). As we can see from what has been written, the discount rate and cash flow are important indicators of the discounting technique and their calculation is mandatory during economic calculations. A separate article about calculating market returns.

Finally, let's look at a simple example of company stocks. Suppose the payment of a certain share at the current value of 1000 rubles was 15% per annum, i.e. 150 rubles. The investor considers such a profit very attractive and agrees to even a smaller amount, up to 9% per annum. This minimum level of income that suits him can also be called the discount rate. Having made the calculation: 150 rubles / 0.09 = 1666.66 rubles, we obtain the upper limit of the price at which it will be profitable for an investor to purchase a share in order to ensure a profitability not lower than the desired one. If the share price decreases, then the current percentage of payments will give a smaller absolute value of profit - for example, with a share price of 900 rubles, 15% per annum will give 135 rubles of profit. But the investor bought the share for 100 rubles cheaper. At the same time, the obvious difficulty is that the dividend payment is not a constant value - in the next period it may be much lower or absent altogether.

Excursion into history

In economic theory, terms such as "discounting", "discount" and "discount rate" are used quite widely and can have several meanings. On the one hand, the word discount (English) is literally translated as the result of calculation and, accordingly, the concept is interpreted as the results of the calculations carried out or the final result. At the same time, the word “discount” can mean a discount or the amount by which the cost of a product will be reduced for a specific buyer. We are interested in the first value.

The term “discount rate” was first used in the 70s, during the emergence of a new model for assessing capital assets ( Capital Asset Pricing Model). The author of this model was economist U. Sharm. The technique was used to determine future stock returns using the capitalization method.

Gradually, the indicator began to be used to assess the profitability of investments in a certain period of time. Today, for a debt-free cash flow, the discount rate is calculated based on the weighted average cost of equity and borrowed capital, without taking into account changes in the amount of borrowed funds in a given period.

Meaning and Use of Discount Rate

Unfortunately, when we are dealing with a real market and stocks, an accurate calculation of a company's future profitability becomes impossible, since we are forced to use certain assumptions to forecast the company's cash flows. There are three options: cash flow can decrease, remain the same, or increase. This means, for example, we can assume growth of 5% per year. Moreover, in addition to the assumption about the amount of cash flow, to calculate the real value of the stock, you also need to know (assume) the P/FCF indicator - it shows how much free cash flow the analyzed company will (should) be worth. For example, a ratio of 15 indicates a company value of 15 cash flows. See free cash flow.

Finally, the value of a stock depends on its future number. Let's say there are 500,000 shares priced at $15 each, forecast to be $20 in five years. Let's say it comes true and the company should be worth 500,000 × 20 = 10 million dollars. However, the company has issued additional shares - if their number is 166,666, then the price of each should remain around the previous $15 mark. Therefore, we should not forget that our assumptions are “hardwired” into the exact calculation figures - so the calculation remains in the realm of probability and is not a guarantee of future profit or loss.

The rate forecasting technique is used in the following cases:

when there is a sufficient amount of information that makes it possible to calculate future profits

if there is an assumption that financial flows in the future will have a different value

Differences in discounting in Russia and the West

If there is a sufficient level of development of the stock market in the country, the discount rate is used as an indicator of the weighted average price of capital - WACC. In Russia, this indicator can only be applied to the debts of a small number of companies - public issuers of securities. To assess risks, a basic risk-free discount rate is used.

In Russian practice, analysts do not discount cash flows, as indicated in the discounting theory, but incomes. The income items are:

net cash flow after deducting all necessary expenses and investments;

net operating income, provided that there are no debts in any area of assessment;

profit that will be taxed.

To calculate the indicator, the cost approach is predominantly used, since it is the simplest and most understandable.

In the West, the discount rate, in addition to the CAPM model, is usually determined in one of the following ways (however, there are at least a dozen in total):

A cumulative construction technique in which the rate acts as one of the risk functions and is calculated as the total amount of risk for a specific object.

A method for comparing alternative investments. Used when calculating the investment price of an object.

Selection method. As part of the methodology, transactions with similar objects are analyzed.

Monitoring method. It consists of constantly monitoring market conditions and forming its main indicators.

Conclusion

As shown above, depending on the problem, the discount rate can mean the value of the bank deposit rate, the amount of inflation, and the amount of expected income from investments. In the latter case, the value of the rate can be taken arbitrarily, calculating the real value of the shares with the projected cash flow in the next 5, 10 or 15 years - however, the higher the rate is (i.e., the higher the expectations), the lower the real price of the stock will be relative to its current prices. In the case of accurate rate data (bank deposits or bond coupons, as well as historical inflation), it is possible to accurately estimate the discounted value. Although the calculation of the discount rate for a specific company can be done in several ways, each of them carries certain assumptions - so the result obtained should be considered only as a forecast, which may not come true.

One hundred rubles today and one hundred rubles in a year are completely different things. By investing money today, we would like to receive a certain income tomorrow. To calculate it, you need a coefficient, and to calculate it, you first need to know what discounting is. We will talk about this below.

Discounting

Discounting is the reduction of future profits (cash flows) to their present (current) value. In other words: discounting is the calculation of the value of money taking into account temporary factors, namely, how much a ruble spent today will be worth in a year. This calculation will allow you to know whether the expected earnings are sufficient. After all, we want the profit to cover the following factors:

- Inflation.

- Risk factors.

- Higher than the return on other investments (deposit).

Example: we have 500 rubles, we invest them in some business, after a while we plan to return 800 rubles. To invest or not? First, let's compare the estimated amount of income brought to today and the available money. To do this we need a discount factor. The desired percentage of profit for the year is 30%, we consider:

- 100% + 30% : 100 = 1.3 (coefficient)

- 800: 1.3 = 615.38 (rub)

The estimated income is greater than the amount received, which means the project is profitable.

Discount rate

What is the discount rate? This is a value expressed as a percentage that reflects the value of monetary units taking into account risk factors and time. This is a variable value that depends on many factors. It is individual for each enterprise, but in general it will look like this:

- i = f(i 1 ,...,i n),

where i 1 is the cost of an alternative investment for this period of time, i n are other factors (inflation and other risk factors). In principle, nothing complicated. And everyone can use these calculations.

Let's touch on such a complex economic term as the discount rate, consider existing modern methods for calculating it and areas of use.

Discount rate and its economic meaning

Discount rate (analog: comparison rate, rate of return)- This is the interest rate that is used to reestimate the value of future capital at the current moment. This is done due to the fact that one of the fundamental laws of economics is the constant depreciation of the value (purchasing power, cost) of money. The discount rate is used in investment analysis when an investor decides about the prospect of investing in a particular object. To do this, he reduces the future value of the investment object to the present (current). By conducting a comparative analysis, he can decide on the attractiveness of the object. Any value of an object is always relative, so the discount rate acts as the basic criterion with which the effectiveness of an investment is compared. Depending on different economic objectives, the discount rate is calculated differently. Let's consider existing methods for estimating the discount rate.

Methods for estimating discount rates

Let's consider 10 methods for estimating the discount rate for evaluating investments and investment projects of an enterprise/company.

- Capital Asset Valuation Models CAPM;

- Modified capital asset valuation model CAPM;

- Model by E. Fama and K. French;

- Model M. Carhart;

- Constant Growth Dividend Model (Gordon);

- Calculation of discount rate based on weighted average cost of capital (WACC);

- Calculation of discount rate based on return on equity;

- Market multiplier method

- Calculation of discount rate based on risk premiums;

- Calculation of the discount rate based on expert assessment;

Calculation of discount rate based on the CAPM model

Capital Asset Pricing Model – CAPM ( CapitalAssetPricingModel) was proposed in the 70s by W. Sharp (1964) to estimate the future return on shares/capital of companies. The CAPM model reflects future returns as the return on a risk-free asset and a risk premium. As a result, if the expected return on a stock is lower than the required return, investors will refuse to invest in this asset. Market risk was taken as a factor determining the future rate in the model. The formula for calculating the discount rate using the CAPM model is as follows:

where: r i – expected return on the stock (discount rate);

where: r i – expected return on the stock (discount rate);

r f – return on a risk-free asset (for example: government bonds);

r m – market return, which can be taken as the average return on the index (MICEX, RTS - for Russia, S&P500 - for the USA);

β – beta coefficient. Reflects the riskiness of the investment in relation to the market, and shows the sensitivity of changes in stock returns to changes in market returns;

σ im – standard deviation of changes in stock returns depending on changes in market returns;

σ 2 m – dispersion of market returns.

Advantages and disadvantages of the CAPM capital asset pricing model

- The model is based on the fundamental principle of the relationship between stock returns and market risk, which is its advantage;

- The model includes only one factor (market risk) to estimate the future return of a stock. Researchers such as Y. Fama, K. French, and others have introduced additional parameters into the CAPM model to increase its forecasting accuracy.

- The model does not take into account taxes, transaction costs, opacity of the stock market, etc.

Calculation of the discount rate using the modified CAPM model

The main disadvantage of the CAPM model is its one-factor nature. Therefore, the modified capital asset pricing model also includes adjustments for unsystematic risk. Unsystematic risk is also called specific risk, which appears only under certain conditions. Calculation formula for modified CAPM model (ModifiedCapitalAssetPricingModel,MCAPM) is as follows:

![]() where: r i – expected return on the stock (discount rate); r f – return on a risk-free asset (for example, government bonds); r m – market return; β – beta coefficient; σ im is the standard deviation of the change in stock returns from the change in market returns; σ 2 m – dispersion of market returns;

where: r i – expected return on the stock (discount rate); r f – return on a risk-free asset (for example, government bonds); r m – market return; β – beta coefficient; σ im is the standard deviation of the change in stock returns from the change in market returns; σ 2 m – dispersion of market returns;

r u – risk premium, including the company’s unsystematic risk.

As a rule, experts are used to assess specific risks because they are difficult to formalize using statistics. The table below shows various risk adjustments ⇓.

| Specific risks | Risk adjustment, % |

| Government influence on tariffs | 0,4% |

| Changes in prices for raw materials, materials, energy, components, rent | 0,2% |

| Management risk of the owner/shareholders | 0,2% |

| Influence of Key Suppliers | 0,3% |

| The influence of seasonality in demand for products | 0,4% |

| Conditions for raising capital | 0,3% |

| Total adjustment for specific risk: | 1,8% |

For example, let’s calculate the discount rate taking into account adjustments, so if according to the CAPM model the yield is 10%, then taking into account risk adjustments the discount rate will be 11.8%. Using a modified model allows you to more accurately determine the future rate of return.

Calculation of the discount rate using the model of E. Fama and K. French

One of the modifications of the CAPM model was the three-factor model of E. Fama and K. French (1992), which began to take into account two more parameters that influence the future rate of profit: company size and industry specifics. Below is the formula of the three-factor model of E. Fama and K. French:

where: r – discount rate; r f – risk-free rate; r m – profitability of the market portfolio;

SMB t is the difference between the returns of weighted average portfolios of small and large capitalization stocks;

HML t is the difference between the returns of weighted average portfolios of shares with large and small ratios of book value to market value;

β, si, h i – coefficients that indicate the influence of parameters r i, r m, r f on the profitability of the i-th asset;

γ is the expected return of an asset in the absence of the influence of 3 risk factors on it.

Calculation of the discount rate based on the M. Karhat model

The three-factor model of E. Fama and K. French was modified by M. Carhart (1997) by introducing a fourth parameter to assess the possible future return of a stock - moment. The moment reflects the rate of price change over a certain historical period of time; when the fourth parameter is used in the model for estimating the profitability of a stock in the future, it is taken into account that the future rate of return is also affected by the rate of price change. Below is the formula for calculating the discount rate using the M. Carhart model:

where: r – discount rate; WMLt – moment, rate of change in the value of a stock over the previous period.

Calculation of the discount rate based on the Gordon model

Another method for calculating the discount rate is to use the Gordon model (Constant Growth Dividend Model). This method has some limitations on its use, because in order to estimate the discount rate, it is necessary that the company issues ordinary shares with dividend payments. Below is the formula for calculating the cost of equity capital of an enterprise (discount rate):

Where:

Where:

DIV – the amount of expected dividend payments per share for the year;

P – share placement price;

fc – costs of issuing shares;

g – dividend growth rate.

Calculation of discount rate based on weighted average cost of capital WACC

Method for estimating the discount rate based on the weighted average cost of capital (eng. WACC, Weighted Average Cost of Capital) one of the most popular and shows the rate of return that should be paid for the use of investment capital. Investment capital can consist of two sources of financing: equity and debt. Often, WACC is used both in financial and investment analysis to estimate the future return on investment, taking into account the initial conditions for the return (profitability) of investment capital. The economic meaning of calculating the weighted average cost of capital is to calculate the minimum acceptable level of profitability (profitability, profitability) of the project. This indicator is used to evaluate investments in an existing project. The formula for calculating the weighted average cost of capital is as follows:

![]()

where: r e ,r d – expected (required) return on equity and debt capital, respectively;

E/V, D/V – share of equity and debt capital. The sum of equity and borrowed capital forms the company’s capital (V=E+D);

t – profit tax rate.

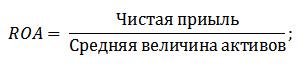

Calculation of discount rate based on return on equity

The advantages of this method include the ability to calculate the discount rate for enterprises that are not listed on the stock market. Therefore, to evaluate the discount, return on equity and debt capital indicators are used. These indicators are easily calculated from balance sheet items. If an enterprise has both equity and borrowed capital, then the indicator used is return on assets. (Return On Assets, ROA). The formula for calculating the return on assets ratio is presented below:

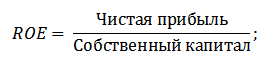

The next method for estimating the discount rate through return on equity is (Return On Equity, ROE), which shows the efficiency/profitability of capital management of an enterprise (company). The profitability ratio shows what rate of profit the company creates using its capital. The formula for calculating the coefficient is as follows:

Developing this approach in assessing the discount rate through assessing the return on capital of the enterprise, a more accurate indicator can be used as a criterion for assessing the rate - return on capital employed (ROCEReturnOnCapitalEmployed). This indicator, unlike ROE, uses long-term liabilities (through shares). This indicator can be used for companies that have preferred shares on the stock market. If the company does not have them, then the ROE ratio is equal to ROCE. The indicator is calculated using the formula:

Another type of return on equity ratio is return on average capital employed ROACE. (Return on Average Capital Employed).

In fact, this indicator corresponds to ROCE, its main difference is the averaging of the cost of capital employed (Equity capital + long-term liabilities) at the beginning and end of the period being assessed. The formula for calculating this indicator:

The ROACE indicator can often replace ROCE, for example, in the EVA economic value added formula. Let us present an analysis of the feasibility of using profitability ratios to estimate the discount rate ⇓.

Calculation of discount rate based on expert assessment

If you need to estimate the discount rate for a venture project, then using the CAPM, Gordon model and WACC methods is impossible, so experts are used to calculate the rate. The essence of expert analysis is a subjective assessment of various macro, meso and micro factors affecting the future rate of profit. Factors that have a strong influence on the discount rate: country risk, industry risk, production risk, seasonal risk, management risk, etc. For each individual project, experts identify their most significant risks and evaluate them using scoring. The advantage of this method is the ability to take into account all possible investor requirements.

Calculation of discount rate based on market multipliers

This method is widely used to calculate the discount rate for enterprises that issue ordinary shares on the stock market. As a result, the market E/P multiplier is calculated, which is translated as EBIDA/Price. The advantages of this approach are that the formula reflects industry risks when valuing a company.

Calculation of discount rate based on risk premiums

The discount rate is calculated as the sum of the risk-free interest rate, inflation and risk premium. As a rule, this method of estimating the discount rate is carried out for various investment projects where it is difficult to statistically estimate the amount of possible risk/return. Formula for calculating the discount rate taking into account the risk premium:

![]() Where:

Where:

r – discount rate;

r f – risk-free interest rate;

r p – risk premium;

I – inflation percentage.

The discount rate formula consists of the sum of the risk-free interest rate, inflation and the risk premium. Inflation was singled out as a separate parameter because money depreciates constantly; this is one of the most important laws of economic functioning. Let us consider separately how each of these components can be assessed.

Methods for estimating the risk-free interest rate

To assess the risk-free value, financial instruments are used that provide profitability with zero risk, that is, absolutely reliable. In reality, no instrument can be considered absolutely reliable; it’s just that the probability of losing money when investing in it is extremely small. Let's consider two methods for estimating the risk-free rate:

- Yield on risk-free government bonds (GKOs - government short-term zero-coupon bonds, OFZs - federal loan bonds) issued by the Ministry of Finance of the Russian Federation. Government bonds have the highest safety rating, so they can be used to calculate the risk-free interest rate. The yield on these types of bonds can be viewed on the website of the Central Bank of the Russian Federation (cbr.ru) and on average it can be taken as 6% per annum.

- US 30-year bond yield. The average yield on these financial instruments is 5%.

Methods for estimating risk premium

The next component of the formula is the risk premium. Since risks always exist, their impact on the discount rate should be assessed. There are many methods for assessing additional investment risks; let’s look at some of them.

Methodology for assessing risk adjustments from the Alt-Invest company

The Alt-Invest methodology includes the following types of risks in the risk adjustment, presented in table ⇓.

Methodology of the Government of the Russian Federation No. 1470 (dated November 22, 1997) for assessing the discount rate for investment projects

The purpose of this methodology is to evaluate investment projects for public investment. Specific risks and adjustments for them will be calculated through expert assessment. To calculate the base (risk-free) discount rate, the refinancing rate of the Central Bank of the Russian Federation was used; this rate can be viewed on the official website of the Central Bank of the Russian Federation (cbr.ru). Specific project risks are assessed by experts in the presented ranges. The maximum discount rate using this method will be 61%.

| Risk-free interest rate | |

| WITH refinancing rate of the Central Bank of the Russian Federation | 11% |

| Risk premium | |

| Specific risks | Risk adjustment, % |

| Investments to intensify production | 3-5% |

| Increasing product sales volume | 8-10% |

| The risk of introducing a new type of product to the market | 13-15% |

| Research costs | 18-20% |

Methodology for calculating the discount rate Vilensky P.L., Livshits V.N., Smolyak S.A.

| Specific risks | Risk adjustment, % |

| 1. The need to conduct R&D (with previously unknown results) by specialized research and (or) design organizations: | |

| duration of R&D less than 1 year | 3-6% |

| R&D duration over 1 year: | |

| a) R&D is carried out by one specialized organization | 7-15% |

| b) R&D is complex in nature and is carried out by several specialized organizations | 11-20% |

| 2. Characteristics of the technology used: | |

| Traditional | 0% |

| New | 2-5% |

| 3. Uncertainty in demand volumes and prices for manufactured products: | |

| existing | 0-5% |

| New | 5-10% |

| 4. Instability (cyclicality, seasonality) of production and demand | 0-3% |

| 5. Uncertainty of the external environment during the implementation of the project (mining, geological, climatic and other natural conditions, aggressiveness of the external environment, etc.) | 0-5% |

| 6. The uncertainty of the process of mastering the technique or technology used. Participants have the opportunity to ensure compliance with technological discipline | 0-4% |

Methodology for calculating the discount rate by Y. Honko for various classes of investments

Scientist J. Honko presented a methodology for calculating risk premiums for various classes of investments/investment projects. These risk premiums are presented in aggregate form and require the investor to select an investment objective and a risk adjustment accordingly. Below are aggregated risk adjustments based on investment objective. As you can see, as the amount of risk increases, the enterprise/company’s ability to enter new markets, expand production and increase competitiveness also increases.

Summary

In the article, we looked at 10 methods for estimating the discount rate, which use different approaches and assumptions in the calculation. The discount rate is one of the central concepts in investment analysis; it is used to calculate indicators such as: NPV, DPP, DPI, EVA, MVA, etc. It is used in assessing the value of investment objects, shares, investment projects, and management decisions. When choosing an assessment method, it is necessary to take into account the purposes for which the assessment is being made and what the initial conditions are. This will allow for the most accurate assessment. Thank you for your attention, Ivan Zhdanov was with you.

Discounted value(Discounted cash flow, DCF) is the present value of future (expected) cash payments to the current point in time. Discounting cash flows is based on the important economic law of diminishing value of money. A sum of money received today usually has a higher value than the same amount received in the future. This is due to the fact that money received today can bring income in the future after its investment. In addition, money received in the future in conditions depreciates (decreases, i.e., with the same amount in the future, fewer goods and services can be purchased). There are also other factors that reduce the cost of future payments. The inequality of monetary amounts at different times is expressed numerically in .

Present value is widely used in economics and finance as a tool for comparing streams of payments received at different times. The discounted value model allows you to determine how much financial investment an investor is willing to make to obtain a given cash flow. The present value of a future stream of payments is a function of the discount rate, which can be determined depending on:

- profitability of alternative investments;

- cost of attracting (borrowing) funds;

- inflation;

- the period over which the future flow of payments is expected;

- the risk associated with a given future stream of payments;

- other factors.

The present value indicator is used as the basis for calculating the amortization of financial borrowings.

The process of discounting value is carried out using both simple and compound interest.

When calculating the amount of simple interest in the process of discounting value (i.e., the discount amount), the following formula is used:

Where D- the discount amount determined by simple interest for the specified period of time as a whole;

S

n- the number of separate periods for which the calculation of interest payments is provided;

i

In this case, the present value of funds (financial instrument), taking into account the calculated discount amount, is determined by the formulas:

Where R

S- future value of funds (financial instrument);

D

n

i- the discount rate used, expressed as a decimal fraction.

When calculating the present value of funds in the process of discounting them using compound interest, the following formula is used:

Where R s- the present value of funds (financial instrument), discounted at compound interest;

S- future value of funds (financial instrument);

n- the number of separate periods for which the calculation of interest payments is provided in the general stipulated period of time;

i- the discount rate used, expressed as a decimal fraction.

Accordingly, the discount amount in this case is determined by the formula:

D s = S - R sWhere D s- the amount of discount determined at compound interest for the specified period of time as a whole;

S- future value of funds (financial instrument);

R s- the present value of funds (financial instrument), discounted at compound interest.

Factor  called the compound interest discount factor.

called the compound interest discount factor.