Movable property: the nuances of taxation. What an accountant needs to know if there is movable property on the balance sheet The tax rate on movable property

Until 2019, movable property was also included in the taxation object (with the exception of movable property, which belongs to depreciation groups 1 and 2 - subclause 7, clause 4, article 374 of the Tax Code of the Russian Federation).

Since 2019, Federal Law No. 302-FZ of August 3, 2018 has excluded movable property from the object of taxation on the property of organizations. Thus, from 2019, the movable property of the organization will not be subject to property tax. This also applies to movable property acquired before 2019. From 2019, only real estate.

The same law N 302-FZ canceled, from 2019, the property tax exemption from movable property (clause 25, article 381 of the Tax Code of the Russian Federation) as it is unnecessary. The need for this benefit has disappeared, since movable property cannot, in principle, be taxed, since it does not belong to the object of taxation.

This exemption will also apply to concession agreements. A concession agreement is a form of partnership between the state and the private sector on mutually beneficial terms, where the government transfers part of its assets and services to the management in order to increase the efficiency of the economy.

Exemption of organizations from tax on all movable property is a measure to reduce tax burden on entrepreneurs and is included in the state tax policy planned for the period from 2020 to 2021, the purpose of which is aimed at depreciation of the main capacities of organizations and a more accelerated introduction of the development of new technologies in the Russian industrial sector.

How to lower now?

There are quite real and legal ways to reduce the property tax of organizations, and without resorting to criminal tricks and direct deception of the state, you only need to know about some of the intricacies of taxation and conflicts of existing legal acts, then you can come to a significant reduction in property taxation.

Property tax minimization methods fall into two categories:

moving an asset to another company (or to an individual entrepreneur) that does not pay tax at all; does not pay it from a specific property or can take advantage of a tax exemption;

decrease in the value of property in accounting.

Legal reduction options tax base:

Due to the decommissioned raw material base, transferred to the needs of production. In any structural enterprise, a policy of writing off the cost of consumables is practiced, and you can apply various ways: according to the first receipt method - the most expensive components are written off, based on the last delivery, using the average calculation of the cost of a certain group of materials. This methodology allows you to write off at the maximum cost of materials spent in production, as a result, the cost of manufactured products increases, and the amount of profit goes to minus. The balance sheet reflects a lower value of assets, which, of course, leads to a significant reduction in property tax.

Due to the revaluation of the value of fixed assets. Many enterprises optimize property taxation using this method, that is, they lead to the restoration of the market value of fixed assets. But there is a certain degree of risk here: it is not realistic to establish the exact market price, since, for example, in different periods the same equipment can vary significantly in value. But if you take into account its lowest value in a certain period, then you can drastically reduce the value of all assets, however, it will be difficult to get by with the involvement of narrow valuation specialists. All this will reduce net asset enterprises, but there is another side of the coin in the form of distrust of investors and creditors. But the tax base will be significantly reduced.

Using the method of conservation of fixed assets. This method is applicable only in one case: when the existing assets are an unbearable tax burden, but it is not advisable to fully realize them, in the future they may become the main material resources. In this case, an order is issued by the management of the enterprise to freeze them, with the obligatory notification of the tax authorities.

Reducing the base based on the inventory. If, during the audit, obsolete, unusable manufactured products, or technological equipment for the production of discontinued products are found, it is subject to write-off, that is, a reduction tax base.

Accounting for obsolete equipment. No one has been using typewriters or computers of the first releases for a long time, but they continue to remain on the balance sheet of the enterprise, therefore, they are subject to taxation. Identified office equipment that does not meet modern requirements can be written off, but in fact it will be possible to use it for some time, until it completely goes out of working order. Here you should deal with the execution of the act of disposal, with the simultaneous posting of valuable spare parts, thereby achieving the goal.

Future Ways to Reduce Property Taxes

Ways to reduce property taxes can include the following:

In the transfer of part of the property rights of a "subsidiary" company operating in tandem with the main enterprise.

Transition to a simplified form of taxation. But not every enterprise can use this method, but only those companies whose annual income does not exceed 15 million rubles.

Reducing costs, and as one of the ways - the purchase of equipment, a fleet of vehicles under a leasing scheme. One feature is visible here: all assets must be listed on the balance sheet of the lessor, otherwise it will not be possible to reduce the actual taxation.

It is allowed to reduce taxation for enterprises engaged in the processing and preservation of agricultural products by river or sea fishing and sea fishing, but on the condition that the share of proceeds from this activity exceeds 70% of the total profit of companies.

Taxation can also be exempted or significantly reduced for those enterprises and companies in which more than 50% of employees have the status of disabled in the state.

Similar concessions are public organizations and cooperatives that involve the labor of disabled people.

At the government level, the collection of property tax from companies belonging to a certain type has been completely abolished. economic activity:

Serving housing and communal services or cultural centers leisure.

Conservationists and environment, fire safety population or civil security issues.

Marine vessels with atomic type engines, pipelines of the main type, railway lines, public highways.

Technical means of satellite communication.

State lands.

A complete list of organizations and companies that can use preferential taxation (read - zero) is closed for publication, and can only be provided to the competent authorities at the request of the court.

Now only real estate will be taxed. As a result, companies received an effective tax planning tool in their hands. In this connection, now is the time to summarize the experience gained by companies in optimizing property tax. Indeed, in practice, quite a lot of ways have been developed to reduce the burden of this tax.

Optimization with rental relationships

With the help of a lease agreement, you can not pay tax on the value of inseparable improvements.

There are reasons to believe that it is possible not to pay property tax from the moment the inseparable improvements are created until the end of the lease agreement. Improvements increase the lessor's property tax base only after they are transferred to the lessor's balance sheet. The tenant does not pay tax, because he does not take them into account in accounting as a fixed asset.

The company leases real estate to a friendly counterparty. The lessee, in turn, makes capital investments in fixed assets with the consent of the lessor. According to the terms of the agreement, they must be accounted for on the balance sheet of the lessor. Civil law also says that such improvements are initially the property of the lessor (clause 4 of article 623 of the Civil Code of the Russian Federation).

However, the landlord does not accept them on his balance sheet until the end of the lease agreement, since he may simply be unaware that inseparable improvements have been made. The tenant, until the end of the contract, does not notify the landlord either about the volume of work performed or about their cost. In this case, the lease term can be arbitrarily long.

When the lease agreement ends, the inseparable improvements are transferred to the landlord, which is formalized by an act. On the date of the transfer act, the owner includes them in his fixed assets. And only from that moment begins to pay property tax.

In addition, when returning inseparable improvements, the tenant may well “forget” to transfer documents confirming the cost of the work to the owner. Therefore, the initial cost of the fixed asset will not increase, as will the property tax base.

In this case, the tax risks fall on the tenant. Since, according to the Ministry of Finance of Russia, from the moment the improvements are put into operation and until they are transferred to the lessor, the balance holder of completed capital investments is the lessee (letters dated 03.11.10 No. -05-01/46, dated 10/24/08 No. 03-05-04-01/37). And until the moment of retirement, he must take into account inseparable improvements on his balance sheet and pay property tax. It should be noted that by disposal officials mean the end of the lease agreement. A similar opinion is shared by the judges of the Supreme Arbitration Court of the Russian Federation (determination of March 26, 2012 No. VAC-2715/12).

There are two ways to avoid such claims. First of all, do not introduce inseparable improvements into operation until the end of the lease agreement. However, in this case, the parties to the lease agreement under the general regime lose the opportunity to amortize the cost of capital investments in tax accounting. Recall that, depending on whether the improvements are reimbursable or not, either the landlord or the tenant can do this.

Another way to reduce the risk is to make a company a tenant on a special regime, for example, on the simplified tax system with the base “income minus expenses”. Such a company will be released from the obligation to pay property tax (clause 2, article 346.11 of the Tax Code of the Russian Federation). At the same time, it has the right to take into account the costs of capital investments.

Liquidation of the object

An object acquired for liquidation or reconstruction does not need to pay tax.

This scheme allows you to save property tax when accounting for objects that do not correspond to the characteristics of fixed assets (clause 4 PBU 6/01).

A company in a shared system acquires a building in progress or a dilapidated building with the intention of tearing it down and building something else in its place. The company formalizes its intention by ordering the demolition or liquidation of property. At the same time, the object is not put into operation, since one of the conditions of PBU 6/01 is not met - there is no ability to generate economic income in the future. Consequently, there is no object of taxation on property tax.

The Ministry of Finance of Russia recognizes that property not intended for use in the company's business activities is not recognized as an object of taxation (Letter No. 03-05-05-01/24 dated April 22, 2008). Arbitration courts also agree with this approach (decisions of the federal arbitration courts of the Volga region of February 20, 2012 No. A55-6362 / 2011 and the North Caucasus of October 13, 2011 No. A53-24208 / 2010 districts).

Real estate objects acquired for reconstruction with a view to subsequent resale are also not subject to taxation (letter of the Ministry of Finance of Russia dated 06.23.09 No. 03-05-05-01 / 36, decision of the Federal Arbitration Court of the Moscow District dated 02.17.10 No. -10). Judges come to a similar conclusion in relation to other real estate, which, for objective reasons, cannot generate income for the company (decisions of the federal arbitration courts of the East Siberian Court dated January 21, 2010 No. A33-11830 / 2008, the West Siberian Court dated April 9, 2010 No. A75 -6674/2009 districts).

Transfer of property into goods

Property planned for sale can be converted to the category of goods and thereby reduce the tax.

The scheme allows you not to pay property tax from the moment when the company ceases to use the objects in its business activities or plans to sell them.

The company decides to sell the property. At the same time, the search for a buyer may take long time. Then, in order to avoid property tax losses, the company transfers it to the category of goods. Since the company has ceased to use the object in its activities and plans to sell it, it is no longer able to generate economic income in the future. This means that it does not meet the criteria of paragraph 4 of PBU 6/01.

In practice, there are examples when judges take the side of taxpayers. According to the arbitrators, the objects that the company ceases to use in its business activities do not meet the criteria for fixed assets. Therefore, they can be excluded from the composition of depreciable property and accounted for as goods for resale (decisions of the federal arbitration courts of the Volga region dated 01.27.09 No. A65-9168 / 2008, Central of 07.04.08 No. A48-3994 / 07-14 districts).

In another case, the judges pointed out that the disputed objects were not used for a long time either in production, or for management needs, or for leasing, and were subsequently sold under a sale and purchase agreement. Therefore, the company rightfully excluded real estate from fixed assets (Resolution of the Federal Arbitration Court of the Volga District dated February 20, 2012 No. A55-6362 / 2011).

Other ways of tax optimization

The amount of property tax depends on the book value of property, plant and equipment and can increase with each purchase of additional assets or their modernization. This makes it difficult for a considerable number of firms to pay large property taxes on time, creating gaps in business. Optimization of property tax is a challenge, as this payment is "direct". In other words, this tax cannot be reduced by certain deductions. We also emphasize that the list of beneficiaries on it is very limited.

When vehicles are considered as an object of taxation, then, in addition to property tax, the organization must pay a transport tax. So, there is a non-observance of the rights of taxpayers associated with double taxation of some objects.

Based on the foregoing, it turns out that the legal optimization of the organization's property tax today is the only effective way its abbreviations.

In this case, taxpayers have several opportunities for optimization. Thanks to them, any enterprise can seriously reduce the tax burden.

Depreciation method

In accounting, depreciation of fixed assets is charged in one of the following ways:

linear;

diminishing balance;

write-offs based on the sum of numbers of years of useful life;

write-offs in proportion to the volume of production.

Most often, accountants use linear variant, since it is much simpler and makes it possible to avoid the formation of a difference between accounting and tax accounting. But if we consider it from the point of view of optimizing the property tax, this method turns out to be the most unsuccessful. With a factor of 2, the diminishing balance method will usually be much more profitable. Therefore, if you want to reduce property tax, calculate depreciation in each of the four methods presented and choose the most profitable one. But of course, linear method should be excluded only if a large difference in the calculations is found.

Application of the simplified taxation system

When working under the simplified system, property tax and some other taxes are replaced by a single tax, with the exception of retail premises, premises of business centers.

Leasing

Companies often purchase fixed assets on credit. To optimize the property tax in such a situation, we recommend considering the option of concluding a leasing transaction. The fact is that it has significant advantages over bank loan. Accounting for the object on the balance sheet of the company that leases it will exempt you from tax for the entire duration of the contract. If the depreciation is fully accrued on the date you acquire title to the asset, you will in principle not have to pay this tax.

If an item is not fully depreciated, it is recorded at a residual value, which is obviously much lower than its original price. Placing a fixed asset on the balance sheet of the lessee allows the use of an accelerated depreciation rate of 3. This exemption also applies to objects that were initially recorded with the lessor and accepted on the balance sheet at their residual value at the end of the contract.

Use of property tax exemptions

This option is considered one of the most time-consuming, so it is not often used to optimize property tax. The reason is that almost all existing benefits are associated with the presence of specific (rather specific) types of property in the company or with the belonging of this enterprise to any industry and the use of property specifically for it. It turns out that optimization should be carried out in advance, even when creating a company and choosing a specific industry for it.

Also, such optimization is long-term in nature, because it will not be easy to reorient later, it will be expensive, and this procedure will take a lot of time. We emphasize that when choosing a field of activity, production, general economic issues are priority, while the possibility of tax optimization is only their addition. But it cannot be denied that the competent application of the benefits offered by the state to business can bring serious benefits.

Revaluation

Any company has a lot of movable objects, whose value is constantly declining. Therefore, obsolete assets that have lost much in value are revalued with the help of expertise in order to reduce property tax. At the same time, tax accounting will be maintained without changes, only the value of fixed assets reflected in the balance sheet will be reduced. This procedure is carried out once a year in relation to groups of homogeneous fixed assets.

In other words, all objects belonging to a certain group, for example, cars, should take part in it. According to the law, it will not be possible to overestimate one of them, while maintaining the previous value of the others. The company itself chooses a specific category of objects, based on economic feasibility. If the price of transport has fallen sharply, while real estate has grown, only cars are revalued, continuing to take into account buildings without changes.

In conclusion, it should be noted that changes in legislation will certainly have a positive effect on the renewal of fixed assets. But at the same time, one should not forget about the existence of effective ways to optimize property taxes.

Property tax for organizations for certain groups of movable property is not paid, and for a number of others it is exempted. Read more about this in our article prepared by the experts of the berator.

In relation to movable property in 2016, the following rules for taxing the property of organizations apply:

- objects included in the first and second depreciation groups are not recognized as an object of taxation in accordance with subparagraph 8 of paragraph 4 of Article 374 of the Tax Code of the Russian Federation without restrictions, regardless of the date of their acceptance for accounting as fixed assets;

- objects included in the third and higher depreciation groups, accepted for accounting as fixed assets before January 1, 2013, are taxed in the general manner;

- objects included in the third and higher depreciation groups, accepted for accounting as fixed assets after January 1, 2013, are exempt from taxation on the basis of paragraph 25 of Article 381 of the Tax Code of the Russian Federation, provided that they are not received as a result of reorganization (liquidation) or from interdependent persons;

- objects included in the third and higher depreciation groups, accepted for accounting as fixed assets after January 1, 2013 (including in 2013 and 2014), received

into an organization as a result of reorganization (liquidation) or from interdependent persons, are taxed in the general manner.

Thus, organizations are exempted from taxation by the property tax of organizations in respect of movable property, accepted from January 1, 2013 for accounting

as fixed assets, with the exception of movable property accepted

into account as a result:

- reorganization or liquidation legal entities;

- transfers, including acquisitions, of property between persons recognized as

in accordance with the provisions of clause 2 of Article 105.1 of the Tax Code of the Russian Federation, they are interdependent.

These restrictions apply in the case of placing objects of movable property

to the balance sheet as a fixed asset in accordance with paragraph 4 of PBU 6/01 “Accounting for fixed assets” (approved by order of the Ministry of Finance of the Russian Federation of March 30, 2001 No. 26n).

Nuances of applying the current benefit

If the movable property accepted on the balance sheet as a result of the reorganization is not taken into account as fixed assets, after its transfer to fixed assets, the restriction

in terms of the impossibility of applying benefits to transactions between related parties

not valid (letter of the Federal Tax Service of Russia dated April 18, 2016 No. BS-4-11/6740).

EXAMPLE

The organization received young animals from a related person. According to the rules accounting it is reflected on account 11 "Animals for growing and fattening". After the transfer of animals to the main herd, they are reflected in fixed assets. After such a transfer, the organization will be able to apply the corporate property tax exemption in the general manner.

The Ministry of Finance of Russia in a letter dated February 9, 2015 No. 03-05-05-01 / 5111 explains that bringing the name of the organization in line with the Civil Code cannot be considered

as a reorganization. This means that there are no grounds for refusing to apply tax benefits.

on property, in the case when movable property was registered as a fixed asset from January 1, 2013. From January 1, 2015, movable property that was registered as fixed assets during 2013-2014 is deprived of benefits as a result of reorganization.

Letter No. 03-05-05-01/5030 of February 6, 2015 of the Ministry of Finance of the Russian Federation clarified that the property tax exemption provided for by paragraph 25 of Article 381 of the Tax Code can be applied even if the property is received from the municipality. Justification - paragraph 5 of Article 105.1 of the Tax Code. Direct and (or) indirect participation Russian Federation, subjects of the Russian Federation, municipalities in Russian organizations, in itself, is not a basis for recognizing such organizations as interdependent.

And in the letter of the Federal Tax Service of the Russian Federation of March 13, 2015 No. ZN-4-11 / 4037 it is said that fixed assets made from materials purchased after January 1, 2013

from an interdependent person are not subject to corporate property tax.

After all productive reserves, from which the fixed asset is made, are not subject to property taxation on the basis of Article 374 of the Tax Code.

Another situation. Under the construction contract, the contractor independently purchases equipment requiring installation and performs installation work.

Then the finished movable property is transferred to the customer, who is an interdependent person with the contractor. As indicated by the Federal Tax Service of Russia in a letter dated July 8, 2016 No. BS-4-11 / 12245, the exemption from property tax established by clause

25 Article 381 of the Tax Code of the Russian Federation does not apply to such movable property.

Vehicles manufactured after January 1, 2013

There is a bill introduced by the Government of the Russian Federation (No. 1155134-6), if adopted, the scope of the benefit established by paragraph 25 of Article 381 of the Tax Code of the Russian Federation will be significantly expanded from January 1, 2017.

Its essence is that organizations that have cars on their balance sheet, produced starting

from January 1, 2013, they will no longer pay personal property tax on them. That is, any vehicle owned by the company, manufactured since January 1, 2013,

exempt from property tax. The restriction on non-application of the benefit in the event of the purchase of a car from a related party or as a result of a reorganization will be removed. The date of manufacture of the machine will be determined by its registration certificate. It will serve as the basis for the exemption.

The bill does not provide for recalculation and refund of tax for previous years.

As a reminder, the 2016 property tax return deadline has expired.

March 30, 2017.

1. Organizations on DOS(including separate divisions with a separate balance sheet), which have fixed assets on their balance sheet that are recognized as an object of taxation for property tax.

2. Organizations on the simplified tax system and UTII, owning .

3. Organizations on ESHN for some property.

Corporate property tax: real estate

All real estate is subject to this tax, except for land plots and other objects of nature management (clause 1, clause 1, clause 4, article 374 of the Tax Code of the Russian Federation).

Moreover, real estate taxation has its own peculiarities. So, organizations on DOS must pay property tax in relation to:

- real estate listed on the balance sheet as fixed assets;

- residential real estate that is not accounted for according to accounting data as fixed assets.

Organizations on the simplified tax system and UTII pay tax (clause 1 of article 378.2 of the Tax Code of the Russian Federation) if they own:

- , for example, shopping centers or premises in them. A complete list of such real estate is given in paragraph 1 of Art. 378.2 of the Tax Code of the Russian Federation;

- residential real estate, which is not accounted for on the balance sheet according to accounting data as a fixed asset.

Organizations on the Unified Agricultural Tax pay tax on property that is not used in the production of agricultural products, primary and subsequent (industrial) processing and sale of these products, as well as in the provision of services by agricultural producers (clause 3 of article 346.1 of the Tax Code of the Russian Federation).

Corporate property tax: movable property

The tax on movable property has not been paid since 01/01/2019 (Federal Law of 08/03/2018 No. 302-FZ).

Corporate property tax: tax base

As a general rule, the tax base is the average annual value of the property, but in relation to the tax is calculated based on its cadastral value (Art. 375, 378.2 of the Tax Code of the Russian Federation).

Property tax of legal entities: reporting periods

Reporting periods for property tax depend on the tax base (clause 2, article 379 of the Tax Code of the Russian Federation):

By the way, regional authorities may not establish reporting periods(Clause 3, Article 379 of the Tax Code of the Russian Federation).

Tax period for property tax

The tax period for the property tax of organizations is the same for all (regardless of the value of the property, on the basis of which the tax is calculated) and is equal to a calendar year (clause 1, article 379 of the Tax Code of the Russian Federation).

Corporate property tax rate

Regional authorities have the right to set the property tax rate themselves, but its amount cannot exceed the rate established by the Tax Code (clause 1, article 380 of the Tax Code of the Russian Federation). This rate is generally 2.2%.

At the same time, it is allowed to establish differentiated tax rates depending on the categories of taxpayers or property recognized as an object of taxation (clause 2, article 380 of the Tax Code of the Russian Federation).

If the regional authorities have not set their own corporate property tax rates, then the tax is calculated based on the rates specified in the Tax Code of the Russian Federation (clause 4, article 380 of the Tax Code of the Russian Federation).

Calculation of corporate property tax

The tax calculation based on the average annual value of the property differs from the tax calculation based on the cadastral value.

And here it is important to note that when calculating the tax based on the average annual value, it is not necessary to take into account real estate, the tax in respect of which is calculated based on the cadastral value.

Calculation of advance payments and tax based on the average annual value of the property

To calculate the advance, you will need to determine the average value of the property (clause 4 of article 376 of the Tax Code of the Russian Federation):

Having determined the average value of the property, you can calculate the amount of the advance payment (clause 4 of article 382 of the Tax Code of the Russian Federation):

To calculate the annual tax amount, you need to determine the average annual value of the property:

The tax calculation looks like this:

At the end of the year, you need to pay extra to the budget by the amount calculated according to the formula:

Calculation of advance payments and tax based on the cadastral value of the property

To understand how much advance payment you need to pay to the budget, you need to make the following calculation (clause 12, article 378.2 of the Tax Code of the Russian Federation):

The annual tax amount is determined by the following formula:

And the amount of tax payable at the end of the year is calculated as follows:

Deadline for paying corporate property tax

The deadline for paying property tax is established by the laws of the constituent entities of the Russian Federation (clause 1, article 383 of the Tax Code of the Russian Federation).

For example, owners of Moscow property must pay tax at the end of the year no later than March 30 of the year following the reporting year (clause 1, article 3 of the Law of the City of Moscow dated 05.11.2003 N 64). And the deadline for payment for payers of property tax in the Republic of Tatarstan is April 5 of the year following the reporting year (part 3, article 4 of the Law of the Republic of Tajikistan dated November 28, 2003 No. 49-ZRT).

Deadline for payment of advance property tax payments

The deadlines for the payment of advance payments, as well as the deadline for paying taxes, are established regional authorities. And, accordingly, in different regions, these terms may be different.

Submission of reporting on corporate property tax

Payers of property tax must submit reports on this tax in the following terms:

| Type of reporting | When it appears | Submission deadline |

|---|---|---|

| Calculation of the advance payment for property tax (Appendix No. 4 to the Order of the Federal Tax Service of March 31, 2017 No. ММВ-7-21/271@) | According to the results of the reporting periods | Not later than the 30th day of the month following the reporting period (clause 2, article 386 of the Tax Code of the Russian Federation) |

| Declaration (Appendix No. 1 to the Order of the Federal Tax Service of March 31, 2017 No. ММВ-7-21/271@) | At the end of the year | Not later than March 30 of the year following the reporting year (clause 3 of article 386 of the Tax Code of the Russian Federation) |

If reporting periods are not established in your region, then, accordingly, you only need to submit a declaration at the end of the year to the Federal Tax Service Inspectorate.

It is not necessary to submit a calculation and a declaration if the organization does not have taxable property.

The nuances of payment and reporting

Organizations must pay advances/tax at the location of the property:

| Property location | Where is the tax paid? |

|---|---|

| The property is located at the location of the organization (clauses 3, 6 of article 383 of the Tax Code of the Russian Federation) | In the IFTS, where the organization is registered |

| The property is located at the location of a separate subdivision with a separate balance sheet (Article 384 of the Tax Code of the Russian Federation) | In the IFTS, where the OP is registered |

| Real estate is located outside the location of the organization and the EP (Article 385 of the Tax Code of the Russian Federation) | In the IFTS serving the territory where the property is located |

The same procedure applies to reporting on property tax (clause 1, article 386 of the Tax Code of the Russian Federation).

If the organization owned the property for less than a year

If taxable property was registered not from the beginning of the reporting year or retired during the year, then this fact will not affect the formula for calculating advances/tax based on the average annual value of the property.

If we are talking about property, the tax in respect of which is calculated on the basis of the cadastral value, then advances / tax are calculated taking into account the ownership ratio (clause 5, article 382 of the Tax Code of the Russian Federation). This coefficient is determined by the following formula:

When calculating the number of full months of ownership, you need to consider that:

- if the ownership of cadastral real estate arose before the 15th day of a particular month inclusive, then this month is taken as a full month. If the right to real estate arose after the 15th day of the month, then this month is not taken into account;

- if the ownership of cadastral real estate is terminated after the 15th day of the month, then this month is included in the calculation of the coefficient as a full month. If the right is terminated before the 15th day of the month inclusive, then such a month does not need to be taken into account.

Since 2018, the rules for calculating property tax on movable fixed assets registered since January 01, 2013 have changed. This article will tell you what the essence of these innovations are and what explanations were given by officials.

You will also learn:

- where and how to specify the tax rate in 1C for movable property;

- how to find out if the "movable" benefit is preserved in your region;

- at what rate to calculate the tax if the benefit is no longer valid;

- how to reflect in the benefits in 1C and in tax reporting.

Tax rates on movable property

From January 01, 2018, the federal benefit established by paragraph 25 of Art. 381 of the Tax Code of the Russian Federation, which exempted movable property registered from 01/01/2013 from tax, has been canceled. However, it can be preserved, but only if the relevant law is adopted by the constituent entities of the Russian Federation (clause 1, article 381.1 of the Tax Code of the Russian Federation).

In those constituent entities of the Russian Federation, whose laws do not provide for a privilege on movable property and the rate is not indicated, it is necessary to pay a tax at a rate of 1.1% (Letter of the Federal Tax Service of the Russian Federation of December 20, 2017 N BS-19-21 / 327). Whether benefits or reduced rates are provided for your region, you can check on the official website of the tax service

By letter N BS-4-21/5834@ dated March 28, 2018, the Federal Tax Service of the Russian Federation brought to its subdivisions the Letter of the Ministry of Industry and Trade of the Russian Federation dated March 23, 2018 N OV-17590-12, which clarifies the issue of classifying fixed assets as movable and immovable property.

Machinery and equipment named in the OKOF in section 330.00.00.00.000 "Other machines and equipment, including household inventory and other objects", located both in the building and outside it, even if attached to the building on the foundation, are considered movable property, as they perform independent production functions.

From 2018, the following rates for property taxation are applied to movable property registered from 01/01/2013:

- the maximum rate of 1.1% - if the regional law does not establish benefits, lower rates, or the maximum rate is set;

- reduced rate, in accordance with the amount established by regional law;

- reduced rate or benefit for individual objects, according to regional laws;

- exemption from property tax, i.e. exemption has been preserved by regional law.

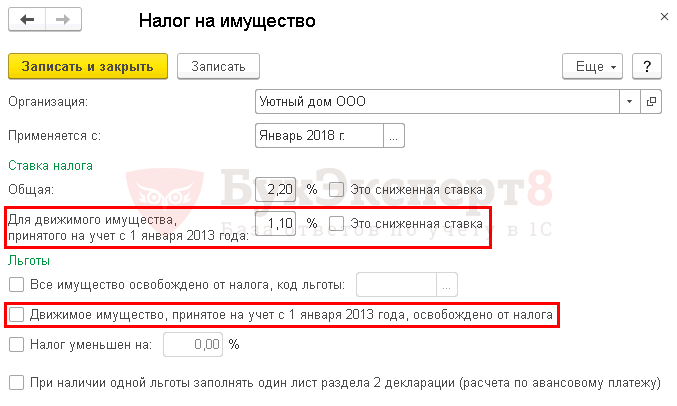

Property tax rates in 1C

Property tax rates for an organization are indicated in the section Directories - Taxes - Property tax - link Rates and benefits.

After updating to release 3.0.57, the program automatically sets a new property tax rate for movable property, which has been in effect since 2018 and is set at federal level(clause 3.3 of article 380 of the Tax Code of the Russian Federation). If a different rate is set by the region, then it must be set manually in the information register Property tax.

If it is necessary to set a different rate or benefit for individual property objects, then for these fixed assets it is necessary to set the settings in information register Property tax: Objects with a special taxation procedure In chapter Directories - Taxes - Property tax - link Objects with a special taxation procedure.

Benefit (rate) code in the property tax return

If a regional law provides for a benefit or a reduced rate for property tax, then, depending on the article of the Tax Code of the Russian Federation, on the basis of which the benefit or rate is granted, a code is determined (Appendix No. 6 "Tax Benefit Codes" to the Procedure for filling out tax return and advance payment for corporate property tax, approved. Order of the Federal Tax Service of the Russian Federation of March 31, 2017 N ММВ-7-21/271@).

The correct setting in 1C of rates and benefits for property tax will ensure the correct automatic filling of the declaration and advance payments. For each benefit code, fill in separate sheet Section 2.

If the region provides benefits with codes:

- 2012000 "tax incentives for tax established by the laws of the constituent entities of the Russian Federation, except for tax incentives in the form of a reduction in the rate and in the form of a reduction in the amount of tax";

- 2012400 "tax benefits for tax ... in the form of a reduction in the tax rate for a certain category of taxpayers";

- 2012500 "tax benefits for tax ... in the form of a reduction in the amount of tax payable to the budget",

then in the declaration after such codes, through a slash, you must manually indicate the data of the law of the subject of the Russian Federation, which has the benefit (Letter of the Federal Tax Service of the Russian Federation dated March 14, 2018 N BS-4-21/4786@).

This must be done in the format:

- article,

- paragraph,

- subparagraph

4 characters are allocated for each value. Unused characters are indicated by zeros.

Consider in detail the options for taxing movable property.

Benefit saved

Let us analyze the features of calculating the tax on movable property while maintaining benefits using the example of Moscow.

In the information register Property tax necessary:

- check the box Movable property registered on January 1, 2013 is exempt from tax .

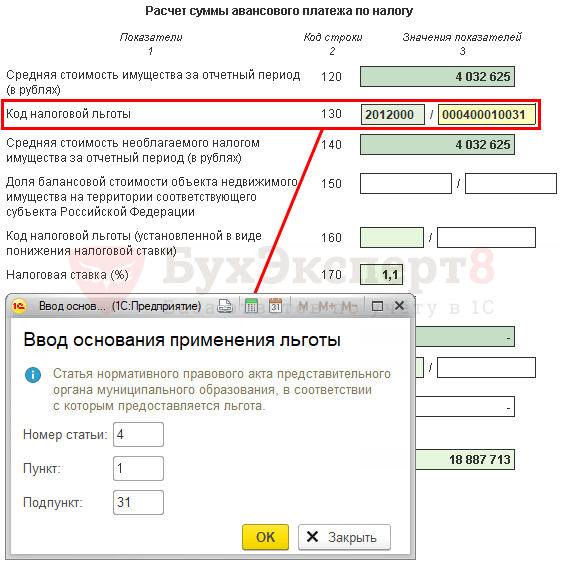

In the declaration (calculation of advance payments) for property tax in pages 160 (130) of Section 2, the code of the benefit and the law under which it is granted are manually indicated:

- instead of a benefit code 2010257 the code is indicated 2012000 “Additional property tax benefits established by the laws of the constituent entities of the Russian Federation ...”;

- fill in the data of the law of the subject of the Russian Federation 000400010031 . In our example, the benefit is granted on the basis of paragraphs. 31 p. 1 art. 4 Law of the city of Moscow dated 05.11.2003 N 64.

Benefit retained partially

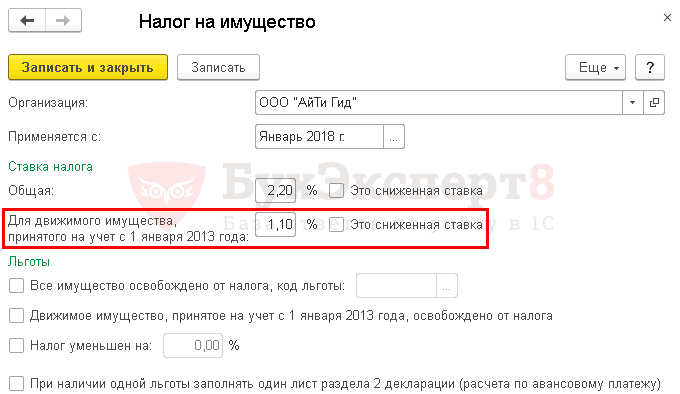

And now let's consider the features of calculating the tax on movable property, if the exemption is retained only for a certain number of movable property, using the example of St. Petersburg.

In the information register Property tax nothing needs to be changed:

- — 1,1

- checkbox This is a reduced rate. not installed.

In order to establish whether movable property falls under this benefit, it is necessary to determine its age, i.e. the number of years that have passed since the year the property was issued.

In 1C, for property objects for which a benefit is established, it is necessary to fill in information in the form Property tax: an object with a special taxation procedure.

- tax credit — Exempted from taxation, the exemption applies, because the date of issue of the car is 08.10.2016 and from this date no more than 3 years have passed; PDF

- Tax benefit code — 2012000 .

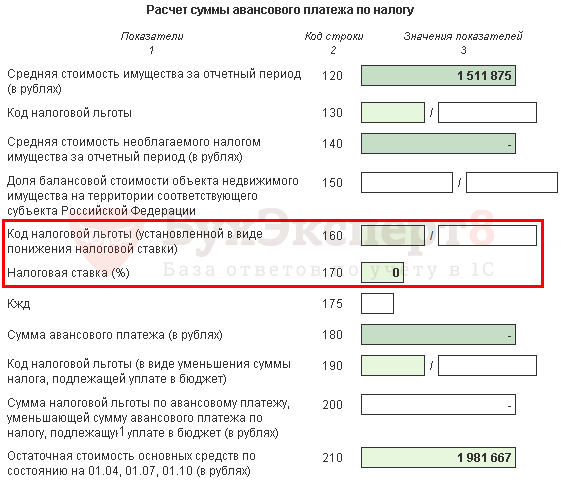

Declaration (calculation of advance payments) for property tax

In the declaration (calculation of advance payments) for property tax in pages 160 (130) of Section 2, the code of the benefit and the law under which it is granted are indicated:

- automatically fill in the benefit code 2012000 "Additional property tax benefits established by the laws of the constituent entities of the Russian Federation ...".

- manually fill in the data of the law of the subject of the Russian Federation 04-100010024 . In our example, the benefit is granted on the basis of Art. 4-1 p. 1 p. 24 Law of the city of St. Petersburg dated November 26, 2003 N 684-96.

Reduced rate, incl. 0%

The amount of the tax rate is established by federal or regional law. Be sure to clarify in the law of your region how the authorities approved the benefit - this is very important for filling out the report.

The subject of the Russian Federation can establish:

- reduced tax rate, incl. 0%;

- reduced rate benefit.

If a reduced or zero rate is mentioned in the regional law in the "Rates" section, the benefit code is not affixed!

Let us consider the features of calculating the tax on movable property if a reduced tax rate is used, using the example of the Moscow Region, in which a simply reduced rate is set, and the Tyumen Region, in which the reduced rate is set as a benefit.

Reduced rate

In the information register Property tax necessary:

- For movable property registered from January 1, 2013 - install 0% ;

- checkbox This is a reduced rate. do not install, because the reduced rate is not set as a benefit.

Declaration (calculation of advance payments) for property tax

- pp. 210 (170) " tax rate (%)» — 0.

Reduced rate as a benefit

In the information register Property tax necessary:

- For movable property registered from January 1, 2013 - install 0,55% ;

- checkbox This is a reduced rateA installed, because in the Tyumen region, a privilege in the form of a reduced rate has been established.

Declaration (calculation of advance payments) for property tax

In the declaration (calculation of advance payments) for property tax, on page 200 (160) of Section 2, the code of the benefit established in the form of a reduction in the tax rate and the law under which it is granted are indicated:

- automatically fill in the benefit code 2012400 "Tax benefits for tax established by the laws of the constituent entities of the Russian Federation in the form of a reduction in the tax rate for a certain category of taxpayers."

- manually fill in the data of the law of the subject of the Russian Federation 0004 0000 0000 . In our example, the reduced rate is set on the basis of Art. 4 Law of the Tyumen region dated October 24, 2017 N 74.

Benefit not saved, rate 1.1%

Consider the features of the calculation of the tax on movable property, if the benefit is not saved, using the example of the Samara region.

In the information register Property tax nothing needs to be changed:

- For movable property registered from January 1, 2013 — 1,1 %, i.e. default value;

- checkbox This is a reduced rate. not installed.

Declaration (calculation of advance payments) for property tax

Section 2 of the declaration (calculation of advance payments) for property tax will be completed in the usual way:

- p. 160 (130) "Tax benefit code" - not filled out;

- line 200 (160) “Tax benefit code (established in the form of a reduction in the tax rate)” - not filled out;

- p. 210 (170) "Tax rate (%)" - 1.1;

- p. 220 (180) "Tax amount (advance payment amount)" - the amount of the calculated tax (advance payment).

In 2018, the objects of taxation by property tax for Russian organizations in the general case, movable and immovable property is recognized, which is accounted for in the organization's accounting as part of fixed assets (clause 1, article 374 of the Tax Code of the Russian Federation).

With regard to movable property accepted for accounting as fixed assets from 01/01/2013 (except for those received from related parties or as a result of reorganization or liquidation), the Tax Code of the Russian Federation provides tax break(Clause 25, Article 381 of the Tax Code of the Russian Federation). At the same time, from 01/01/2018, this benefit is valid in a particular subject of the Russian Federation only if it is provided for by the relevant law of the subject (clause 1, article 381.1 of the Tax Code of the Russian Federation).

So, for example, in Moscow, the tax on movable property 2018 provides for the above benefit (clause 31, part 1, article 4 of the Law of Moscow dated 05.11.2003 No. 64). And, say, in the Tver region, the privilege for movable property does not apply (Law of the Tver region dated November 27, 2003 No. 85-ZO).

Of course, a benefit for movable property can be provided for objects of 3-10 depreciation groups. After all, movable fixed assets included in 1 or 2 depreciation groups are not subject to taxation at all (clause 8, clause 4, article 374 of the Tax Code of the Russian Federation).

However, while the current topic of the tax on movable property of organizations in 2018, from next year will lose its importance. This is due to the fact that the Law on the abolition of the tax on movable property has been adopted.

There will be no tax on movable property from 2019!

From 01/01/2019, paras. "a" paragraph 19 of Art. 2 federal law dated 03.08.2018 No. 302-FZ. Changes are made to paragraph 1 of Art. 374 of the Tax Code of the Russian Federation, where the concept of the object of taxation is given. The word “movable” has been excluded from the definition of the object of taxation by property tax. That is, from 2019, only real estate can be taxed on property.

Thus, from 01/01/2019, the tax on movable property has been abolished in relation to such objects, regardless of the date of their acquisition, or the method or source of receipt of movable property.

Please note that until 01/01/2019, exempted movable property, although not taxed, is reflected in the declaration (calculation) for property tax in section 2 in the subsection devoted to calculating the average annual (average) value of property. In addition, privileged movable property and even movable fixed assets of I-II depreciation groups (which, in principle, are not recognized as an object of taxation for property tax) are referenced in the declaration, calculation in lines 270, 210, respectively. From 01/01/2019, the value of movable property in the declaration (calculation) for property tax will not be shown either for settlement or reference purposes.